The fight over the future of Affordable Care Act (ACA) subsidies escalated sharply on Capitol Hill this week as Senate Republicans rolled out their own health-care proposal, setting up dueling votes Thursday on competing Democratic and Republican plans. With enhanced ACA subsidies scheduled to expire at the end of the year, the chamber is hurtling toward a pivotal showdown—one in which both measures are widely expected to fail but will shape the negotiations that follow.

The Republican plan, authored by Sens. Mike Crapo of Idaho and Bill Cassidy of Louisiana, offers a fundamentally different approach to health-care assistance, seeking to replace the premium tax subsidies with a two-year program that would direct federal payments straight into health savings accounts (HSAs). By contrast, Democrats are pushing a clean, three-year extension of the enhanced subsidies that have existed since the pandemic. The stakes are particularly high as average 2026 ACA premiums have already increased roughly 26 percent, intensifying pressure from constituents and heightening political sensitivities heading into an election year.

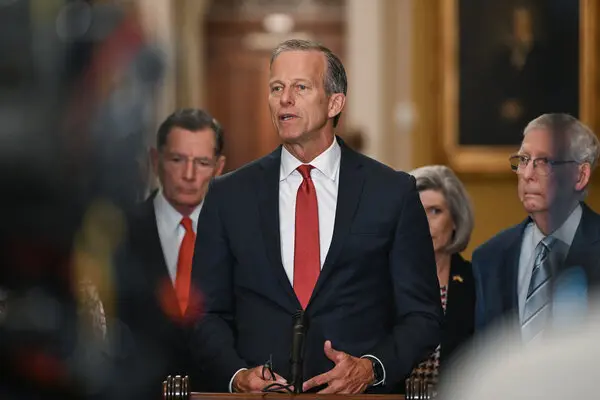

Senate Majority Leader John Thune, flanked by senior Republican leadership including Sens. Shelley Moore Capito, John Barrasso, and Tom Cotton, positioned the GOP plan as a patient-centric alternative that prioritizes cost control and fiscal restraint. “It delivers the benefit directly to the patient, not the insurance company, and it does it in a way that actually saves money,” Thune said. Republicans have long criticized the ACA subsidy structure as distortionary, arguing that subsidizing premiums artificially sustains high insurance prices and creates limited incentive for cost reduction among providers and insurers.

Under the Republican bill, individuals aged 18 to 49 who earn up to 700 percent of the federal poverty level—approximately $225,000 for a family of four in 2025—would receive $1,000 paid directly into an HSA. Those aged 50 to 64 would receive $1,500. The subsidy would then be paired with specific ACA marketplace health plans, giving participants more direct control over their healthcare spending but reducing federal involvement in premium structures.

While the HSA component is the centerpiece of the GOP proposal, the legislation also contains policy provisions that have already sparked fierce partisan reaction. First, it limits federal Medicaid funding to states that extend coverage to undocumented immigrants—a move Republicans argue is necessary to preserve the safety net for legal residents. Second, it bars federal Medicaid funding from being used for gender transition services and excludes those procedures from being defined as essential health benefits for ACA marketplace plans.

Democrats immediately rejected the proposal, calling it both insufficient and ideologically loaded. Senate Minority Leader Charles E. Schumer delivered a blunt assessment, saying, “Their bill is junk insurance. It’s been repudiated in the past. The American people will repudiate it once again.”

The rhetoric underscores the larger political context: Republicans control the chamber 53–47, but neither of the competing proposals is expected to reach the 60-vote threshold needed to overcome a filibuster. Still, both parties view Thursday’s votes as strategically significant. For Democrats, pushing their three-year subsidy extension reinforces their position that healthcare affordability remains one of their core governing priorities. For Republicans, offering an alternative plan shields them from charges—especially harmful in competitive 2026 Senate races—that they have no healthcare strategy of their own.

Behind the scenes, negotiators in both chambers have been scrambling to chart a credible path forward. The ACA subsidies expire on December 31, and without congressional action, millions of Americans could face steep premium spikes or lose insurance altogether. Complicating the timeline further, federal spending itself runs out again after January 31, raising the possibility that subsidy negotiations could become entangled with broader budget brinkmanship and potentially trigger another shutdown standoff.

Roughly 24 million Americans currently depend on the ACA marketplace for health insurance, and most receive the enhanced subsidies that Democrats are seeking to extend. Many of those subsidies originated during the pandemic years, when lawmakers expanded financial assistance to prevent widespread coverage loss during economic disruption. The question facing Congress now is whether those expanded subsidies should become a long-term fixture or be phased out in favor of alternative models.

Republicans argue that their plan modernizes insurance incentives while tempering costs and reducing federal dependency. By channeling money directly into HSAs, rather than insurance companies, they claim their proposal restores consumer choice and injects market pressure into the system. Additionally, the GOP argues that subsidy expiration is overdue. Several Republicans have framed the subsidies as a relic of the pandemic era that must now be replaced with a more sustainable design.

Democrats counter that the Republican plan would leave millions facing higher premiums and restrict access to services based on ideological considerations. They also point out that the GOP’s Medicaid limitations and exclusions related to gender transition services are policy riders that stand no chance of bipartisan support. Beyond those ideological disputes, Democrats insist that the current ACA subsidies have kept healthcare affordable for millions during a period of significant inflationary pressure and that allowing them to expire would be economically and politically irresponsible.

Some moderate Republicans—particularly those up for reelection in states with competitive 2026 Senate races—have privately expressed concern that failure to support some form of subsidy renewal could harm the GOP’s political standing among suburban and middle-income voters who rely heavily on ACA plans. Those concerns have quietly pushed the Republican leadership to produce a counter-proposal that at least signals willingness to negotiate.

Still, as the Thursday vote approaches, neither side expects legislative victory. Both parties anticipate a symbolic but important vote that clarifies negotiating positions ahead of a potential January compromise effort. Several senators on both sides of the aisle have indicated cautious optimism that a middle-ground solution could emerge early next year—one potentially blending elements of direct assistance with limited subsidy continuation. But with the December 31 subsidy deadline fast approaching and election pressures intensifying, crafting such a compromise will require bipartisan coordination that Congress has consistently struggled to achieve.

The broader legislative landscape also adds pressure. The House, under Speaker Mike Johnson, has not committed to holding a healthcare vote before the end of the year. Johnson convened a group of Republican leaders on Tuesday to explore legislative options, but sources indicate no firm timeline has been established. With several competing proposals circulating—at least six in the Senate and two in the House—the window for consensus remains narrow.

If Congress fails to act, many marketplace enrollees could face premium shock as soon as early January. For families already grappling with rising costs, the consequences could be severe. Healthcare economists warn that subsidy expiration could drive younger and healthier individuals out of the marketplace, triggering a destabilizing cycle of rising premiums and shrinking risk pools.

The political optics are equally fraught. Democrats have positioned the subsidy extension as a core affordability issue heading into 2026. Republicans, meanwhile, face the challenge of balancing fiscal conservatism with constituent pressures, all while trying to avoid being blamed for coverage losses in an election cycle where several GOP-held Senate seats are vulnerable.

For now, all attention turns to Thursday’s vote—a legislative clash in which both sides expect defeat but hope to shape the narrative heading into January negotiations. As the deadline looms, the stakes—political, economic, and personal—continue to rise for lawmakers and millions of Americans whose healthcare coverage hangs in the balance.

Emily Johnson is a critically acclaimed essayist and novelist known for her thought-provoking works centered on feminism, women’s rights, and modern relationships. Born and raised in Portland, Oregon, Emily grew up with a deep love of books, often spending her afternoons at her local library. She went on to study literature and gender studies at UCLA, where she became deeply involved in activism and began publishing essays in campus journals. Her debut essay collection, Voices Unbound, struck a chord with readers nationwide for its fearless exploration of gender dynamics, identity, and the challenges faced by women in contemporary society. Emily later transitioned into fiction, writing novels that balance compelling storytelling with social commentary. Her protagonists are often strong, multidimensional women navigating love, ambition, and the struggles of everyday life, making her a favorite among readers who crave authentic, relatable narratives. Critics praise her ability to merge personal intimacy with universal themes. Off the page, Emily is an advocate for women in publishing, leading workshops that encourage young female writers to embrace their voices. She lives in Seattle with her partner and two rescue cats, where she continues to write, teach, and inspire a new generation of storytellers.